The idea of an unconditional basic income looks like a good idea – a plausible extension of the common concept of life-supporting infrastructure — roads, communication, water supply, sanitation, police protection, defense are all part of that concept of providing essential conditions for all citizens.

One of the most frequent arguments is that such a guaranteed basic income would replace dozens of other support programs with their expensive and dignity-destroying bureaucracy, and provide recipients ‘freedom’ to allocate their funds in the way that corresponds best to their different individual needs, and pursue their own creative preferences.

The obvious question of how it would be financed is usually brushed off with that comment on savings from replacement of those programs, and seems to shut off further questions – as well as further investigation and discussion.

Since the devil often hides in the details of such noble endeavors, it seems necessary to look at some of those questions that aren’t being discussed.

At the risk of oversimplification, would it be useful to start with some basic assumptions and a very simple diagram of the main aspects, and their specific implications?

One assumption is that such a Basic Income should be sufficient to support a citizen’s needs for living a reasonably dignified life, providing the essential means for shelter, nourishment, clothing, health care, education, and so on. It should represent an adequate ‘life support’ package of life in a civilized society. Obviously, determining the size of such an income will require some investigation and discussion; it seems that it will not be easy to settle upon one size that will adequately but not extravagantly support residents in all locations, climates, and life situations. But some analysis of basic provisions for such a program it can be assumed as settled somehow.

Another assumption is that it should be ‘universal’ – that is, that all citizens should receive it regardless of their other economic or other situation. So some proposals – such as one providing the income for citizens over 21 years of age – already seem to twist that assumption somewhat.

A somewhat obvious assumption is that this basic income cannot be taxed — it is indeed sometimes being described as a ‘negative income tax’. The obvious implication that it therefore must be financed out of government income from other sources – in an economy consisting only of the components of producing the ingredients of that basic life support bundle, but no further production of ‘luxury’ items that would not be attainable with that income, the government distributing the Basic Income would have to tax everybody’s entire Basic Income to run the program – or just print money, which would end up in the pockets of the producers, and irresponsibly cause unstoppable inflation. But this raises the question of what items should be considered as ‘luxury’ and therefore taxed to supply the revenues for the UBI.

The question of financing might be started — to reveal some disturbing issues — with some very simplified assumption about such an economy. Considering the main components: The population would consist of

1) People who are working and producing – as a first simple assumption, only the ingredients of the basic life support system; let’s call this group ‘P’;

2) People who do not produce anything: ‘NP’;

3) The Government – ‘G’– that distributes the UBI income to everybody (for the sake of simplicity, it could be assumed that this is all done by computers, and that ‘the Government’ would not also consist of people receiving the UBI;

4) An element that might be called ‘Distribution’ – ‘D’ — (it might also be just a ‘machine’; but it is necessary to assume such an institution or ‘market’ where the actual products of the life support package LS can be exchanged for the money of the UBI (and vice versa).

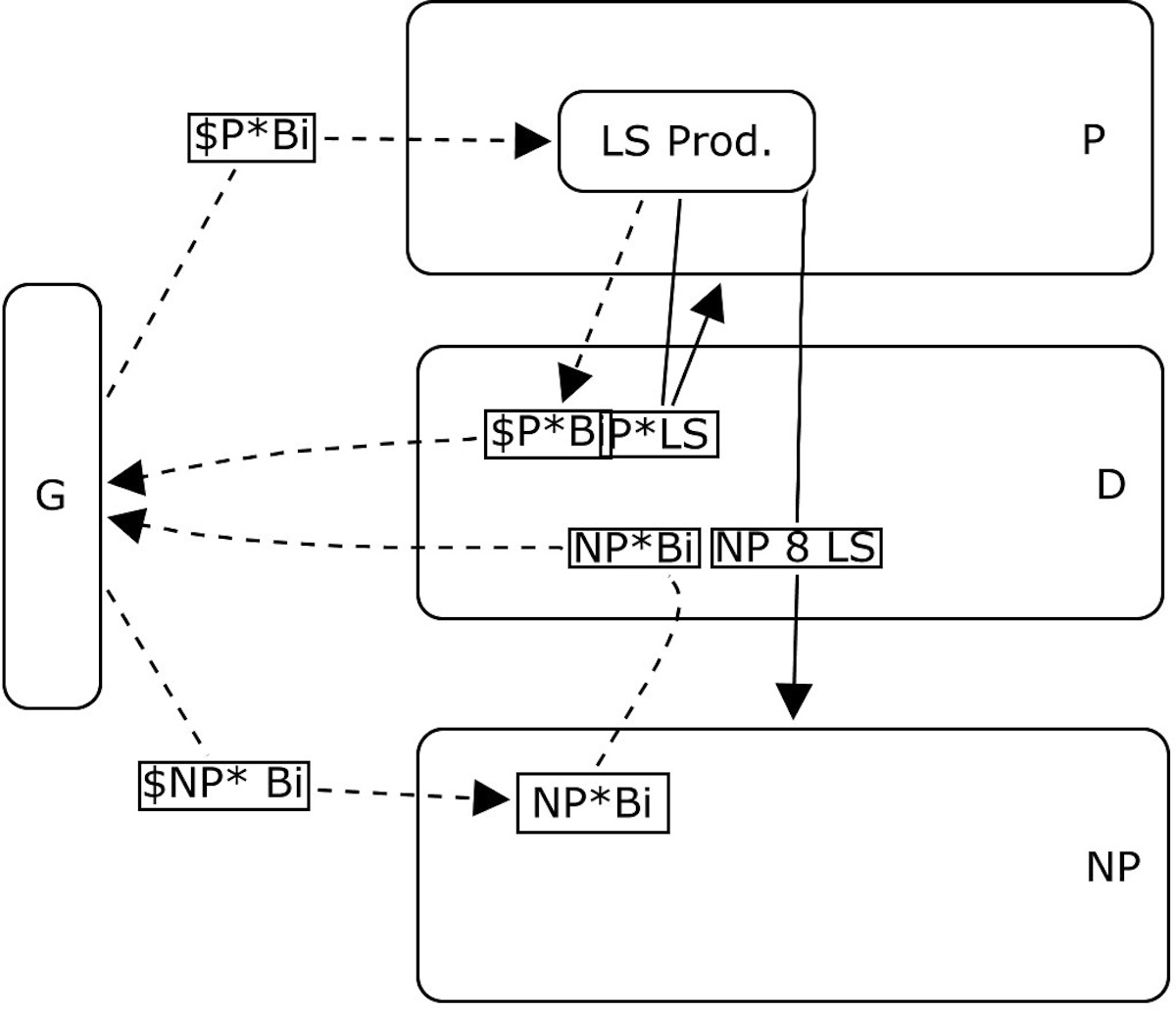

The simple ‘system’ of this economy could now be crudely diagrammed as follows:

Figure 1 UBI ‘self-financed’ with only LS production?

P produces (P+NP)*LS and transfer this to D,

Having receiving $P*Bi from the government, this sum is transferred to D in return for P*LS life support packages (the content of individual packages may differ according to people’s different preferences) but the entire package is P*LS and ‘worth’ $P*Bi; so P’s are ‘paying’ $P*Bi to the distributor D. The P population ‘consumes’ P packages of LS.

NP are receiving $NP*Bi from the government and buy NP*LS worth this much from D, so transferring that sum to D. This part of society ‘consumes’ NP units of LS.

G To be able to pay out the next ‘round’ of Bi payments, the Government must receive the sums $P*Bi + $NP*Bi back from the Distributor D.

So far, so good; this ‘system’ seems to be ‘sustainable’. But is it? What, if anything, is P getting for producing all the life support packages? Just the amount needed for the P people involved in production to stay alive — $P*Bi?

The UBI proponents will argue that the UBI can’t be financed (as the scheme of Fig. 1 does) from the UBI payments: it must come from the production and payments of goods and services NOT in the LS package description: ‘luxury’ items ‘LX’.

The diagram for this arrangement might now look like the following (Fig. 2):

.

Fig. 2 UBI financed (only?) by taxes on ‘Luxury’ products

Now P is producing not only the needed LS packages for everybody in that society, but also an indeterminate amount of ‘luxury’ goods and services. These items are also transferred (sold) to the Distributor D, and then sold back to members of the Producer group P. These people must now have earned some additional funds – of course, from their profits of having produced some of the PX goods. That is, D must have paid them for those. (Shouldn’t they have been paid something for producing the excess number of LS packages for the NP group? This would of course mean that the total sum of payments to P for LS must be larger than $P*Bi – but where does the difference come from?)

If the assumption is to be satisfied that the whole UBI scheme must be financed from the ‘luxury’ items part of the economy, this will determine the total amount of payments—and thus the price of the luxury items – involved in this sector: For the scheme to be viable under the stated assumption, the sum (LX ‘taxes’) to be paid to the government must equal (at least) $ (P+NP)*Bi – regardless of the size of this sector, the number and quality of luxury items produced and sold. Question: How can the UBI-mandated price of a luxury item be established / predicted based on how much it will contribute to the needed government UBI Payments? This seems to fly in the face of standard views of economics, such as that the price for a good or service should be determined by the cost of producing it, a reasonable profit margin, and from then on by demand.

I am sure these and similar questions can be answered by better qualified experts. For example, the overall problem that the viable financing of the UBI system will be inexorably linked to the ratio of P to NP – which is likely to change over time – and therefore likely demand adjustments to those changes even in the amount of UBI payment the government can ‘afford’? or in the purchasing value of those payments – in violation of the ‘guaranteed’ part of the BIG promise of ‘Basic Income Guarantee’?

I’d like to see the proponents of the idea spend some effort in answering these admittedly annoying little detail questions – even to the public who may not have had the chance to review any more detailed proposals than the PR propaganda pieces focusing only on the main ‘reduce government’ and similar arguments. Including questions I have blanked out from this little inquiry: the issue of the resources going into the production of all these goods and services, the question of different amounts of time, skills, education etc. to produce them, and the role of the entire ‘distribution’ segment, including transportation, interim financing, advertising, and selling, the aspect of ‘consumed’ goods (e.g. food’) as opposed to durable goods (houses), and the whole wicked issue of insurance to deal with randomly occurring needs whose costs exceed anybody’s ability to pay for them out of an UBI Payment. It seems that the public discussion of this concept has not covered all pertinent issues yet.

0 Responses to “Some dumb BIG UBI questions from a non-expert”